As Singapore’s climate reporting requirements take full effect, companies designing and building office spaces face a fundamental shift. Workplaces are now strategic assets central to environmental impact, regulatory compliance, and long-term business resilience. For those planning new offices or refurbishments, understanding and responding to these changes is critical to staying competitive and future-proof in a rapidly evolving landscape.

Singapore’s Phased Climate Reporting Framework: What Companies Need to Know

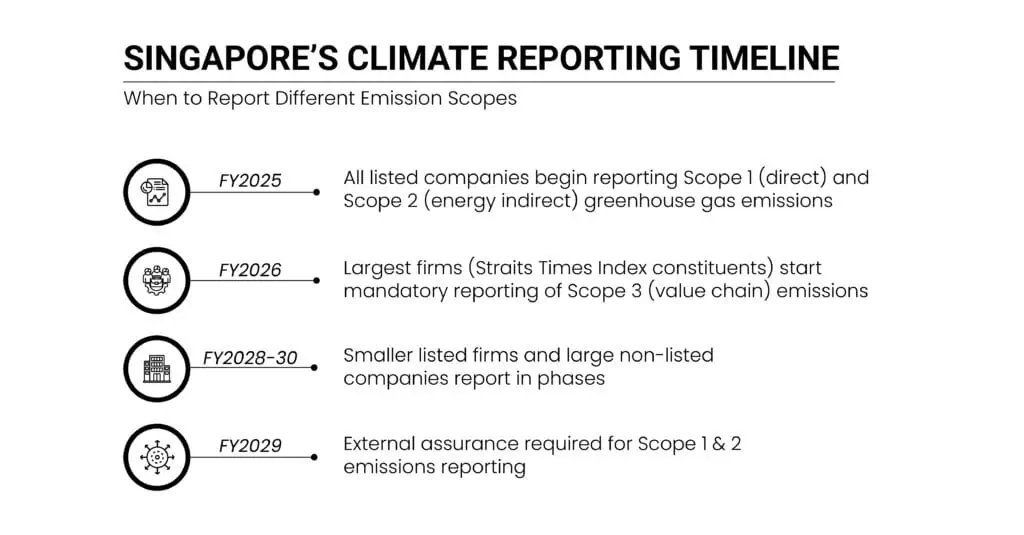

Singapore leads Asia with a staggered, pragmatic climate reporting rollout aligned with global standards. From Fiscal Year (FY) 2025, all listed companies must disclose Scope 1 (direct) and Scope 2 (energy-related indirect) greenhouse gas emissions. The largest firms—primarily Straits Times Index (STI) constituents—will expand mandatory reporting to Scope 3 value chain emissions beginning FY 2026. For smaller listed firms and large non-listed companies, reporting timelines extend to FY 2028–2030, allowing for capacity building and readiness.

External assurance of Scope 1 and 2 emissions reporting is set for FY 2029, increasing data credibility and investor trust. This graduated approach balances compliance costs with Singapore’s firm commitment to transparent, material climate disclosures that underpin its net-zero ambitions.

The Strategic Focus for 2026: Preparing for Expanded Scope 3 Reporting

The upcoming 2026 milestone introduces mandatory Scope 3 emissions reporting for Singapore’s largest companies—an ambitious requirement covering upstream and downstream impacts such as supply chains, construction embodied carbon, employee commuting, and waste management. This calls for:

- Robust data systems extending beyond office boundaries.

- Closely collaborating with suppliers and contractors to collect embodied and lifecycle emissions.

- Applying circular economy principles, emphasizing material transparency and design for adaptability.

- Aligning disclosures with the International Sustainability Standards Board (ISSB) for global comparability.

Companies that proactively prepare for 2026 will reduce regulatory risk, strengthen climate resilience, and enhance ESG credibility with investors and clients.

Designing Workplaces for Singapore’s Climate-Forward Future

Modern workplace design is shifting towards integrated, data-driven ecosystems delivering measurable sustainability and business value. Emerging priorities include:

- Digital twin frameworks enabling real-time simulation and predictive optimization of building performance and occupant impact.

- Future-proof infrastructure designed with capacity for emerging climate technologies such as grid-interactive storage and next-generation HVAC adaptability.

- Material transparency and circular metrics are facilitated by advanced material passports that detail embodied carbon, recyclability, and supply chain documentation, supporting lifecycle impact optimization.

This approach supersedes traditional aesthetics, focusing instead on verifiable, dynamic sustainability outcomes and continuous improvement.

Actionable Strategies for Building Climate-Resilient Workplaces in Singapore

Companies embarking on workplace projects should consider:

- Adopting dynamic energy modeling reflecting live occupancy and consumption patterns to optimize efficiency.

- Integrating lifecycle-informed procurement, evaluating sustainability impact and upcyclability.

- Enabling adaptive reuse through modular design, reducing waste and embodied carbon.

- Expanding performance metrics beyond energy to include water intensity and occupant health indices relevant to productivity.

- Building ESG reporting workflows aligned with ISSB and SGX mandates for streamlined compliance and verification.

In Conclusion

Embedding adaptive design and data-first management is essential to navigating regulatory complexities while unlocking new value streams – be it through operational cost savings, brand differentiation, or resilient risk management.

The landscape from 2024 to 2030 presents challenges and opportunities alike. Companies preparing now for key milestones, especially the pivotal 2026 Scope 3 reporting, place themselves at the forefront of compliance, resilience, and ESG leadership.

At Zyeta, we advocate for viewing workplaces not simply as assets but as agile platforms that evolve with shifting climate policies, technology advances, and workforce expectations. Our commitment is to partner with clients in creating offices that serve today’s needs while anticipating tomorrow’s challenges.

Sources:

ACRA & SGX RegCo. (2025). Joint Press Release: Extended Timelines for Most Climate Reporting Requirements to Support Companies. Singapore: ACRA and SGX RegCo. Available at: https://www.acra.gov.sg/accountancy/sustainability-reporting/overview

IFRS Foundation. (2023). IFRS S2 Climate-related Disclosures. London: ISSB. Available at: https://www.ifrs.org/issued-standards/ifrs-sustainability-standards-navigator/ifrs-s2-climate-related-disclosures/

GHG Protocol. (2011). The Corporate Value Chain (Scope 3) Accounting and Reporting Standard. Washington, D.C.: WRI & WBCSD. Available at: https://ghgprotocol.org/corporate-value-chain-scope-3-standard

SGX RegCo. (2025). Listing Rules, Practice Note 7.7: Sustainability Reporting. Singapore: Singapore Exchange Regulation. Available at: https://rulebook.sgx.com/rulebook/sustainability-report

Related Reads:

How is AI-driven Design Revolutionizing Office Spaces in Singapore?

How is Japandi Design Redefining Workspace Design in Southeast Asia?